OCI Global - Trading at 24% Discount To Proforma Net Cash Amidst Ongoing Strategic Review; Remaining European Nitrogen Business Reflects Additional Upside

OCI Global (OCINF)

1. Company Background

OCI Global (OCI N.V.) is a Dutch public company, headquartered in Amsterdam, the Netherlands. The company is listed on the Euronext Amsterdam stock exchange (AMS) under the stock symbol OCI. The stock trades over-the-counter in the US under the symbol OCINF. As of 11/29/24, the company had an equity market cap of $2.4B (211,357,989 shares outstanding at $11.58/share).

The company is a global producer and distributor of ammonia, nitrate fertilizers, methanol, and hydrogen products and solutions.

The company is at least ~47% owned by the Sawiris family, a wealthy Egyptian family, with Nassef Sawiris (the youngest of three sons of the original founder of the company) currently owning 39% and serving as the Executive Chairman of the Board. Nassef previously served as the company’s CEO through 2020 but no longer holds a management position.

In early 2023, the company launched a strategic review of its assets with the objective of addressing the market discount to the company’s fair value. This strategic review was undertaken in response to calls from activist investor Jeff Ubben’s Inclusive Capital Partners in March 2023 to explore strategic alternatives (Reuters March 2023), citing that the company was worth nearly double its $6B market cap at the time.

Since then, the company has signed four major transactions to offload various businesses, three of which have closed as of November 2024, with the 4th expected to close in first half of 2025. Below is a summary of the transactions.

Source: Q3 2024 Trading Update Presentation (dated 11/12/24)

Following these four transactions, the only remaining business the company will own will be the company’s European Nitrogen business and the remaining corporate-level entities.

Source: 2023 Annual Report

2. Investment Opportunity Summary

As of November 2024, the Company has a net cash position of approximately $2.1B. This follows the most recent closing of the Fertiglobe transaction on 10/15/24 for $3.6B, and an extraordinary shareholder cash distribution the company made on 11/14/24 of $3.3B (EUR 14.50/share).

Proforma for the closing of the 4th transaction (OCI Methanol to Methanex in H1 2025), as well as completion of the company’s OCI Clean Ammonia development in H2 2025 (which will trigger certain deferred compensation to be paid by the buyer, Woodside), the company will hold net cash & securities of approximately $3.2B (or $15.22/share) consisting of the following:

Cash of $3.4B

Shares in Methanex of $450M (9.9 million common shares of a Canadian publicly listed company at $45/share; this is part of the purchase consideration OCI will receive for the OCI Methanol sale to close in H1 2025)

Offset by gross debt of $600M (USD 6.7% bonds maturing in 2033)

This reflects 31% upside from the current market cap of $2.4B ($11.58/share).

In addition to this net cash position, the company will continue to own the EU Nitrogen business, which management is currently exploring strategic alternatives for as part of its strategic review. This business reflects additional upside to the net cash position. Management has guided this business to having “mid-cycle” EBITDA potential of $150M plus. This business is made up of the following:

The company’s nitrogen production assets located in Geleen, the Netherlands. OCI Nitrogen is Europe’s second largest integrated nitrates fertilizer producer and one of the world’s largest melamine producers; and

OCI Terminal Europoort B.V. This is Europe’s only independent ammonia import terminal, located in the port of Rotterdam, and is connected to a well-established multimodal last-mile distribution platform into Europe’s main industrial regions.

Based on further analysis below, I estimate the EU Nitrogen business could be worth an additional $400-750M, which brings total proforma net equity value of the company to $3.6-4.0B ($17-19/share), or 48-62% upside from the current stock price. This upside should be realized in the next 12 months as the company executes on closing the OCI Methanol transaction in H1 2025, completes the OCI Clean Ammonia development project in H2 2025, and potentially signs a transaction with respect to the EU Nitrogen business.

OCI has also guided towards making a further extraordinary cash distribution to shareholders of approximately $1B during H1 2025, subject to continued progress on the execution of the announced transaction and the strategic review, which should assist with closing the current discount reflected in the share price.

Walk from 6/30/24 Actual Net Debt Position to Proforma Net Cash/Securities Position in H2 2025

Source: Company filings, earnings calls, estimates

3. Overview & Valuation of European Nitrogen Business

Business & Assets Overview

The EU Nitrogen business is Europe’s second largest integrated nitrates fertilizer producer and one of the world’s largest melamine producers. In addition, the company owns an ammonia import terminal in the port of Rotterdam, which is connected to a well-established distribution platform into Europe’s main industrial regions.

Nitrogen Production Assets

The European Nitrogen production assets are located in Geleen, the Netherlands. The company has a max production capacity of approximately 3.2 million metric tons of nitrogen products per year (approximately 2.6 million metric tons of fertilizer capacity, and 0.5 million metric tons of other industrial product capacity). The company’s products include:

- Fertilizers

350K metric tons of ammonia. Ammonia is a colorless gas that is a building block for industrial chemicals and nitrogen fertilizers, and can be applied as a direct fertilizer. The principal raw material used in conventional production of ammonia is natural gas, which the company purchases through long term supply contracts.

730K metric tons of UAN (urea ammonium nitrate). UAN is a liquid fertilizer which consists of urea and ammonium nitrate. Due to its nitrate component, it is easily absorbed by plants.

1.6 million metric tons of CAN (calcium ammonium nitrate). CAN, branded as OCI Nutramon, is a nitrogen fertilizer with an addition of dolomite. While the nitrate enables immediate nutrient uptake by crops due to its high absorption properties, the added dolomite reduces soil acidification potential and subsequent liming need.

- Other Industrial Products

222K metric tons of melamine. Melamine is an organic based substance, which consists of 66% nitrogen. Its application lies predominantly within home renovation and construction markets as an intermediate in wood-based panels and a component of glue. OCI Nitrogen Europe is one of the world's largest melamine producers.

300K metric tons of DEF/Adblue (diesel exhaust fluid). DEF/Adblue is a non-hazardous aqueous urea solution consisting of approximately 67.5% deionized water and approximately 32.5% urea.

In terms of competitiveness, OCI is one of the only producers of ISCC (International Sustainability and Carbon Certification) certified renewable ammonia. Renewable and low carbon ammonia can be used to produce lower carbon downstream products. Additionally, OCI’s ammonia production is amongst the most energy efficient in the world, with a gas to ammonia conversion efficiency of 32 MMBtu of natural gas per ton of Ammonia, vs the EU average of 37 MMBtu. This should allow OCI to remain competitive amidst the movement towards (and increased regulations around) lowering carbon emissions.

Rotterdam ammonia import terminal and distribution platform

The company’s ammonia import terminal is the only independent ammonia terminal in Europe, meaning that it has an established 3rd party customer base, and is not exclusively for captive use. The terminal currently has a throughput capacity of 600K metric tons per annum, with an ongoing project to expand to 1.2 million metric tons by end of 2024, and future optionality to expand to 2 million metric tons plus. The terminal is connected to a river and rail distribution network, including ~350 rail tank cars that service 3rd party ammonia customers.

Source: Company filings

OCI believes the Rotterdam terminal will be pivotal in meeting European Union hydrogen targets to decarbonize, as hydrogen imports will need to be imported via ammonia.

Source: Company filings

OCI expects new applications for the use of ammonia in maritime fuels, power generation, and as a hydrogen carrier will contribute to significant demand growth for low-carbon ammonia.

Source: Company filings

Financial Summary

The EU Nitrogen business has historically had a stable earnings profile, earning around $100-250M of EBITDA/year from 2018-2022. Management has guided to a midcycle EBITDA potential of around $150M EBITDA plus in a “normalized gas market”; however this has not been the case since 2021. Natural gas is the primary raw material the company uses to produce its products.

In 2021, natural gas prices began to increase as a result of a drop in Russian gas flows to Europe, as well as generally cold weather directly impacting demand (especially across Asia and Europe). The invasion of Ukraine in February 2022 then caused prices to rise dramatically due to reduced Russian gas supplies, resulting in a severe energy crisis across Europe. Notably, the price of natural gas in the US (Henry Hub), has been significantly lower and more stable in recent years.

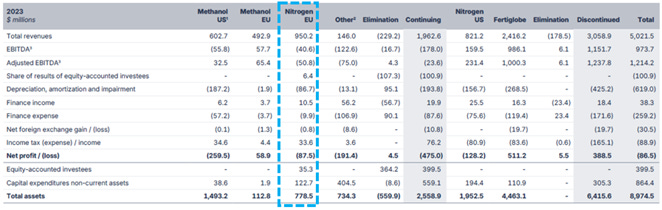

The significant volatility in gas prices is evident in the Nitrogen EU P&L, with adjusted EBITDA bottoming at -$51M in 2023.

Source: Company filings

The most acute impact of the volatility in gas prices is seen in Q4 2022 and Q1 2023 as higher cost inventory (produced at higher cost natural gas) was sold in a lower priced market.

Source: Company filings

Source: Company filings

In the latest Q3 update call in November 2024, management noted “today, despite decent reserves in Europe, there [continues to be] a bit of a geopolitical component affecting [gas] pricing, even though the curve does come down in time, reflecting a more stabilized environment.” While not disclosing specific numbers, management noted adjusted EBITDA for the EU Nitrogen business decreased slightly in Q3 2024 compared to Q3 2023 (which was $16M), in part due to higher natural gas prices. Therefore, adjusted EBITDA is likely end up in the ~$60M range in 2024, still depressed from mid-cycle levels.

Management noted in the same Q3 update call, “As European natural gas prices normalize, the profitability of our European Nitrogen operations is expected to improve significantly, reverting back towards midcycle levels, reflecting the asset's competitive positioning as some of the most energy efficient in Europe.”

Valuation

In terms of valuation for the EU Nitrogen business, I think a rough approximation based on a multiple of EBITDA works for the purpose of this investment case. This remaining business only reflects upside to the investment, given shares already trade at a discount to projected net cash & securities. Management noted as recently as 11/12/24 that it is “actively engaged in the evaluation of strategic alternatives for its European Nitrogen assets in the Netherlands.”

For some context on EBITDA multiples for this type of business, we can look to 5 publicly traded companies that are more or less comparable.

YAR (Yara International) is probably the most comparable – it is based in Oslo (Norway), has similar product offerings of nitrogen-based fertilizers and industrial chemicals, and has a strong presence in the EU market. The other comparables have similar overlap in terms of product offerings but are either more geographically diversified (CF, CF Industries and NTR, Nutrien) or primarily focused on the North American market (LXU, LSB Industries and UAN, CVR Partners).

Following reporting peak earnings for 2022 in early 2023, YAR was trading at around a 3x EV/EBITDA multiple. A similar 3x multiple for the EU Nitrogen business on peak 2022 EBITDA of ~$250M would have put a value on EU Nitrogen in the range of $750M.

Source: Yara International Filings

Alternatively, if we take the more recent multiples for all comps (~6-7x EBITDA) on LTM EBITDA for the EU Nitrogen business of ~$65M, we get to a value of $390-455M.

4. Investment Risks and Rational for Discount

Below are some thoughts around potential drivers of the discount reflected in the current share price.

Execution/legal risk related to closing the sale of OCI Methanol to Methanex

On 9/9/24, OCI signed the agreement to sell 100% of the OCI Methanol business (both the US and European operations) to Methanex, a $3B market cap Canadian publicly traded methanol company. The transaction is expected to close in the 1st half of 2025, subject to legal and regulatory conditions, and relevant anti-trust approvals. OCI will receive gross proceeds of $1.6B, consisting of $1.15B in cash and 9.9 million in newly-issued Methanex stock (approximately $450M at $45/share). Following the transaction, OCI will be the 2nd largest shareholder of Methanex, owning ~13%.

Part of the assets being sold to Methanex include OCI Methanol’s 50% stake in a joint venture called Natgasoline (a methanol production plant in Beaumont, Texas), which is 50% owned by Proman AG, a European based methanol & fertilizer company. Proman has filed a lawsuit concerning shareholder rights in Delaware against OCI. OCI strongly believes that Proman’s claims are without merit and intends to “vigorously defend the case”. In the latest Q3 update call in November, management reiterated the company is confident in its legal position and sees the situation as minimal risk. The company expects to reach a conclusion on the lawsuit consistent with the timing of obtaining final regulatory approvals for the transaction. To the extent the dispute is not successfully resolved by the time regulatory approvals are received, Methanex has the option to not close on the Natgasoline JV, and close only on the remainder of the transaction (in this situation, Methanex would retain the right to acquire the 50% interest in the Natgasoline JV for a certain period of time). Natgasoline represents 40% of the enterprise value consideration of the transaction ($820M based on the transaction enterprise value of $2.05B).

The Natgasoline plant also had an incident in late September with reports that a gas line ruptured (Natgasoline Sep 2024), causing the plant to halt operations. OCI management confirmed the plant is currently down while repairs are underway, with operations expected to resume before the end of the year. OCI expects the repairs to be covered by insurance plus any deductibles.

Overall, these issues seem like relatively minimal risk to the overall investment. In investor calls both management teams of OCI and Methanex have seemed intent on and confident that they will be able to close the full transaction, including the Natgasoline JV stake. However, if the Natgasoline piece does end up getting carved out of the deal, OCI would obviously still retain that asset and look for alternative ways to maximize value from it.

Execution risk related to Clean Ammonia project completion

On 8/5/24, OCI signed the agreement to sell 100% of its equity interests in OCI’s 1.1 million metric tonnes “Clean Ammonia” project under construction in Beaumont, Texas to Woodside Energy Group Ltd, a $30B market cap Australian publicly traded oil and gas company, for a total purchase consideration of $2.35B. The project began engineering in late 2021, construction in December 2022, and is expected to produce first ammonia in 2025. Under the sale transaction, Woodside paid 80% of the purchase price ($1.9B) at the closing of the transaction (which occurred on 9/30/24), and will pay the balance ($470M) at project completion. OCI is continuing the manage the construction, commissioning, and startup of the facility until the project is fully staffed and operational, at which point it will hand over the plant to Woodside.

Since the initial signing of the agreement, OCI has expected to complete the project in the 2nd half of 2025. The project has a total cumulative expected cash spend of $1.55B (“including contingencies”), of which OCI had spent $799M through 9/30/24.

There is some risk here associated with OCI locking in the purchase price of the plant ahead of completing it, as well as with generally meeting the timeline that has been set out. OCI expects $750M of remaining spend to complete the plant between 9/30/24 and 2H 2025 ($1.55B total spend less $799M spent to date through 9/30/24). Management acknowledged in the November update call that they are focused on executing on this (along with closing the Methanex transaction):

“We still have a pretty large transaction to get through in 2025. We have to execute a landmark project in Texas in the form of Clean Ammonia on a very determined schedule.”

It is difficult to say what the chances are that OCI misses its budget or timeline here based on publicly available information. Management did indicate the $1.55B budget “includes contingencies”.

As an order of magnitude, a 10% miss on the overall $1.55B budget would equate to $155M (which seems unlikely given over half of this budget has already been spent through 9/30/24). This compares to the $1.2-1.5B discount to intrinsic value estimated in the current share price ($3.6-4.0B of intrinsic value vs $2.4B market cap). Also at risk would be the $470M to be paid by Woodside to OCI at project completion.

Uncertainty around use of sale proceeds, future strategy, and concentrated ownership

While OCI recently completed a $3.3B extraordinary shareholder distribution, and has guided towards making an additional $1B distribution in 1H 2025, there is still some uncertainty as to how the company will proceed following the closure of the strategic transactions in 2025. Assuming the company executes as expected, it would complete a $1B distribution in 1H 2025 and be left with $2.2B of net cash/securities (including ~$450M of Methanex stock) in 2H 2025, as well as the EU Nitrogen business (to the extent a sale or other transaction is not executed by then).

In a 9/10/24 presentation, OCI management noted it “expects to provide further clarity on the future strategy of OCI around the time of its Q3 results.” Additionally, it noted how the proceeds received from the four strategic transactions to date would provide “material balance sheet flexibility” for “investing in future value accretive investment opportunities” (in addition to achieving a net cash position and meaningful extraordinary shareholder distributions).

In the Q3 update call on 11/12/24, when asked about potential future investments, management responded with the following:

“…obviously, this has been a topic of discussion that's been broached since we started announcing these transactions, including the transformative nature. At this time we continue to be focused on executing a significant amount of work. As you can appreciate, we've announced a lot of transactions in a short period of time. We still have a pretty large transaction to get through in 2025. We have to execute a landmark project in Texas in the form of Clean Ammonia on a very determined schedule. And we continue to do some thinking around the future strategy. But of course, we have taken notes of all of the inbound comments and consideration that investors have in this regard. And as soon as we feel we can share more insights into our thinking, we will do so. I believe, what's important today is that we have efficiently returned a significant amount of capital to shareholder. With the $1 billion of guidance that we expect to distribute, hopefully, in the first half of 2025, this will really take the number up significantly over a period of four years. And that, of course, would not preclude any future distributions as well.”

Further on the Q3 call, management was asked about rationale for keeping the $600M of bonds outstanding (rather than retiring them early as the company has done with the rest of its debt):

Question: “Can you talk about your existing 6.7% bonds outstanding? This doesn't appear to make sense in the context of the run rate EBITDA earnings for European Nitrogen. Why would you not just take out all of the remaining debt?”

Management response: “We we're assessing alternatives for the for the remaining debt in the business in the context of our future capital strategy. And while the outstanding bonds could remain attractive financing for the company, we may consider a further optimization of our capital structure, as we think about our business going forward. So, we'll continue to do some thinking and share our thoughts in the future in this regard.”

Based on this, it sounds like the company is keeping their options open with respect to winding down the business or pursuing new investment opportunities following the current transactions being contemplated. There is some risk/uncertainty here to the extent the company uses the proceeds to make a new investment that the market does not appreciate. However, it’s worth pointing out that the company, despite being significantly controlled by the Sawiris family, has taken into consideration the input of an activist investor, Jeff Ubben, and has acted pretty quickly and decisively to sell off the vast majority of the assets and return the majority of the capital to shareholders.

Depressed state of EU Nitrogen business

Lastly, the discount in the stock price could be driven by the current depressed state of the EU Nitrogen business and instability in European gas markets. To the extent there is some stabilization in these markets, this may help the market to assign a higher value to the business.

As a point of comparison, the Yara International market cap also appears to be at a cyclical low, down about 50% from 2022.

5. Other Items of Note

Ownership

OCI and its predecessor firm, Orascom Group were founded by Onsi Sawiris, an Egyptian billionaire who died in 2021.

The current Executive Chairman of OCI is Nassef Sawiris, the youngest of three sons of Onsi. Nassef owns 39% of the company, has been involved with OCI and its predecessor firm since 1982, and remained CEO of OCI until 2020. Nassef is an Egyptian billionaire (richest man in Egypt with estimated $8B net worth) with diverse other business interests and roles including ownership stakes and board roles at Adidas, Aston Villa (an English Premier League team), and various other companies. Nassef does not currently hold a management role at the company.

Nassef’s older brother, Samih owns ~5% of OCI but is not a current executive or board member of the company. Nassef’s mother, Yousirya Sawiris owns ~3.5% of OCI.

As of 8/6/24, Inclusive Capital Partners (investment firm of activist investor Jeff Ubben) still owned the ~5% stake in OCI that it acquired in March 2023 when it originally called for the company to review strategic alternatives.

Source: Euronext

Disclosure: I own shares of OCI